How Businesses Can Adapt and Thrive Amid Spending Shifts

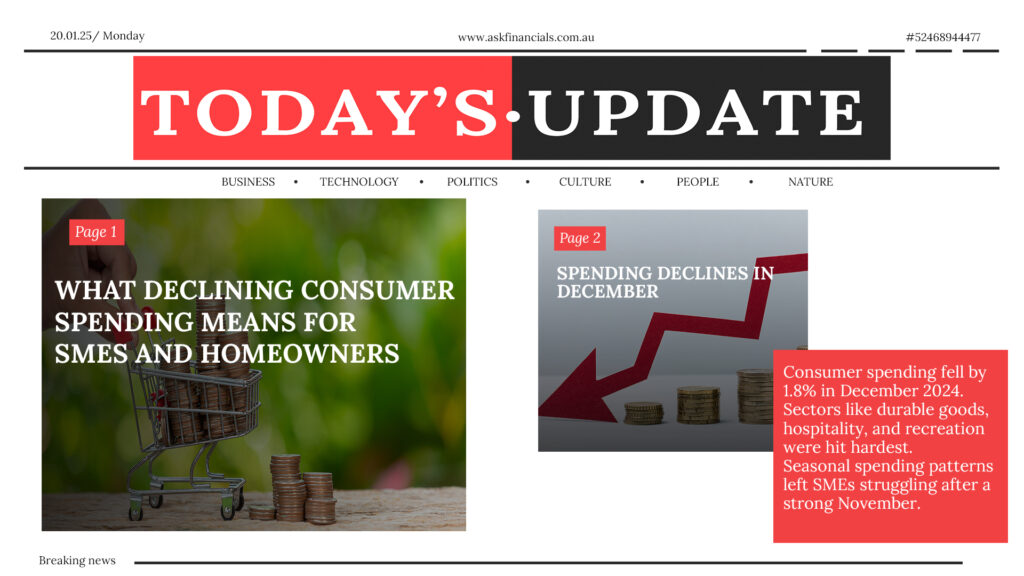

The relaxation of consumer spending posed existential threats to Australia’s small and medium-sized enterprises (SMEs) as they grappled with insolvency crises during December of the year 2024. Data from the CBA House Spending Insights (HSI) Index estimate a 1.8% fall in spending in December, following a strong recovery in November due to Black Friday sales.

The sharpest contraction in household spending occurred with durable goods, suffering an 8.3% slump. In a similar trend, food and beverages, hospitality, and recreation have shrunk by 2.6 %, 2.0%, and 2.0%, respectively. While spending was stronger than anticipated for the year, growing 5.2%, SMEs that heavily relied on seasonal and discretionary spending were not so fortunate as they struggled due to the unsettling distribution of expenditures from the economy.

The main causes of these difficulties are the Southern economy and the change in consumer behaviour brought about by past financial strains.

Over 2024, almost 88% of small and medium-sized companies (SMEs) claimed they suffered from cash flow.

These issues first arose largely in the following forms:

- Income sources lost by 35%,

- insufficient 30% cash reserves,

- variations in demand depending on the season (27%).

After experiencing increased spending in November due to the Black Friday sales, December spending was severely muted.

CBA’s Chief Economist, Stephen Halmarick, said, “With rising costs and uncertainty in the economy, consumers are taking a precautionary approach. This directly harms the household goods, hospitality, and recreation sectors.” They are focusing on need-based purchases and doing away with nonessentials.

As we know, many SMEs can suffer from the lack of discretionary spending due to the economic recession, and in this case, interest rate policies and living expenses packed household budgets tighter than before.

Practical Measures to Tackle Issues: SMEs are starting to tackle these issues.

Some of the most popular methods are:

Cost Reduction: 34% of SMEs claim to be going over their budget and cutting out non-essential costs.

Building Cash Reserves: In anticipation of future expenses, 27% are setting aside money for rainy days.

New Sources of Income: 26% are expanding their products or services to enter or create new markets.

Revising Prices and Efforts in Sales: 25% are revising their prices or spending more resources on advertisements for sales.

However, some businesses depend on self-defeating strategies, such as self-financing expenses (27%). This practice is bound to create more problems later.

Measures such as these are not recommended by the Executive General Manager of Small Business Banking of CBA Rebecca Warren. “Even though it is great to have an overarching vision for SMEs, implementation such as reducing salaries or using personal savings could hurt the owner and the business in the long run.”

Lowering interest rates could assist in improving the overall situation. A Brighter Outlook:

Relief comes from the fact that the Reserve Bank of Australia is anticipated to slash interest rates shortly. All of which means lowered borrowing expenses, greater consumer optimism, and an improved general atmosphere for SMEs. These measures, combined with the reduction of inflation, can put businesses back on their feet by 2025.

ASK Financials understands the unique struggles of SMEs in today’s economic climate. We provide tailored working capital solutions and strategic guidance to help your business thrive, even in tough times.

Book a call with us today and discover how we can strengthen your cash flow, reduce financial stress, and set your business on a path to growth.