Australian Homebuyers and Investors Show Resilience as Mortgage Credit Continues to Climb Amid Rising Borrowing Costs

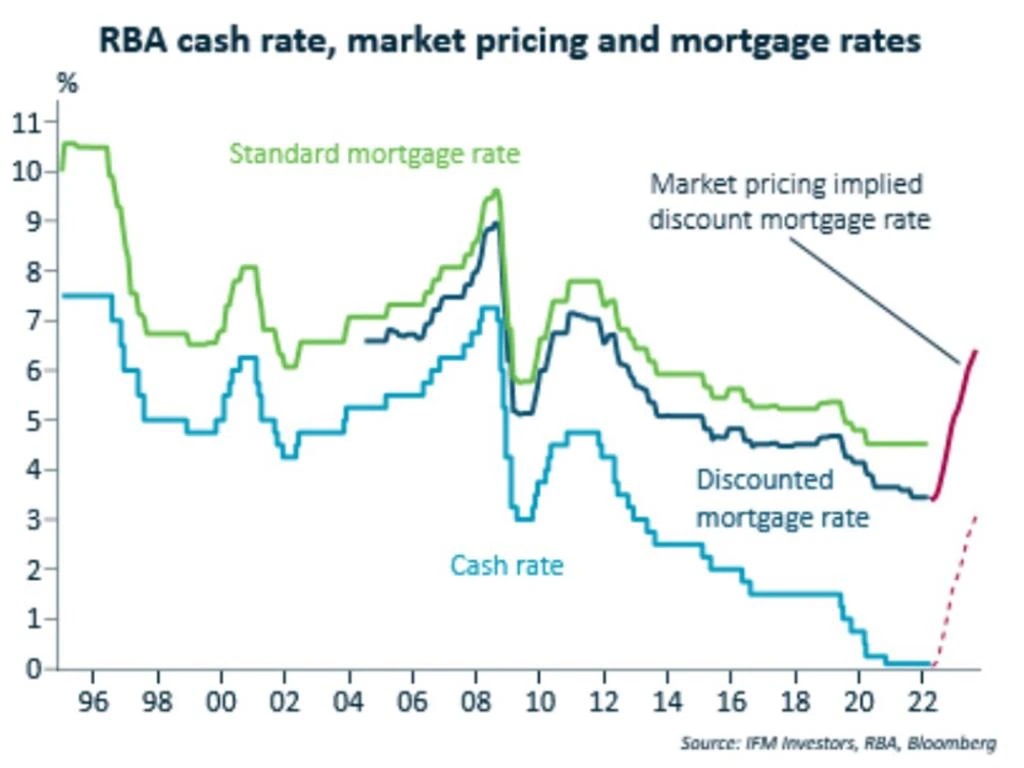

This chart shows the RBA cash rate, standard, and discounted mortgage rates from 1996 to 2022, with rates declining until a sharp rise in 2022. This highlights tightening monetary policy and rising borrowing costs.

Australia’s mortgage market is showing strong growth, even though interest rates have been rising. According to the latest data from the Australian Prudential Regulation Authority (APRA), mortgage credit has continued to increase, defying expectations in the face of higher borrowing costs.

Mortgage Credit Growth Despite High Rates

The latest Quarterly Authorised Deposit-taking Institution (ADI) Performance Report revealed an X% rise in outstanding credit for residential mortgages over the last quarter. This growth comes as a surprise, considering the Reserve Bank of Australia’s (RBA) efforts to raise interest rates to control inflation.

Historically, mortgage markets slow down when interest rates go up, but this time, demand for loans is holding steady. Experts suggest that Australians continue investing in homes and property despite rising costs.

Resilience in Housing Demand

Several factors are contributing to this continued demand. Homebuyers, including first-time buyers, remain active in the market, spurred on by government incentives and a strong desire to own property. Many are also opting for fixed-rate mortgages, which offer stability against the unpredictability of rising rates. With expectations that rates might increase even further, locking in a fixed rate is proving to be a wise move for many.

In addition, certain areas of Australia are still experiencing property price growth, encouraging buyers to act before prices rise further. This has kept the housing market strong, despite the rising costs of borrowing.

First-time Buyers and Investors Driving the Market

The latest report also highlighted that first-time homebuyers and property investors are playing a big part in the continued demand. Despite the added pressure of higher rates, many are still pursuing their homeownership dreams and property investment goals. Some are even borrowing larger amounts to take advantage of the current market conditions before rates go even higher.

Government programs aimed at first-time buyers are helping ease the financial burden, while investors are eyeing opportunities in an ever-changing market, with long-term growth potential in sight.

Risks for the Future of the Market

However, experts caution that the mortgage credit growth we are seeing today may not last forever. Higher interest rates could eventually strain household budgets, especially as mortgage repayments become more expensive. If this continues, it could lead to a slowdown in demand for new loans in the future.

The RBA may also implement more rate hikes if inflation persists, which could make borrowing even more expensive for Australians. As a result, the mortgage market may face challenges as affordability becomes a growing concern.

A Balancing Act for the Housing Market

The surge in mortgage credit highlights the delicate balance between housing demand and interest rates. While current market conditions show resilience, the future remains uncertain. The RBA’s actions, inflation trends, and consumer behavior will all play a critical role in shaping the market over the next year.

While mortgage credit is growing at a steady pace right now, the outlook for the future remains unclear. With rising rates and potential affordability issues on the horizon, buyers and investors need to stay informed and act accordingly.

If you’re considering buying a home or refinancing your mortgage, now may be the time to make a move.

Explore your mortgage options at ASK FINANCIALS by booking a call with us and get expert advice on how to play in the current market conditions. We’re here to help you make the best financial decisions for your future.

Book a free chat to Ask Financials.