Australia’s unemployment rate fell to an all-time low of 3.9% in November 2024, surprising many with its financial resilience and exceeding the Reserve Bank of Australia’s (RBA) forecast of 4.3%. Although this decline represents a healthy functioning market and an enhanced financial system, it creates challenges for debtors.

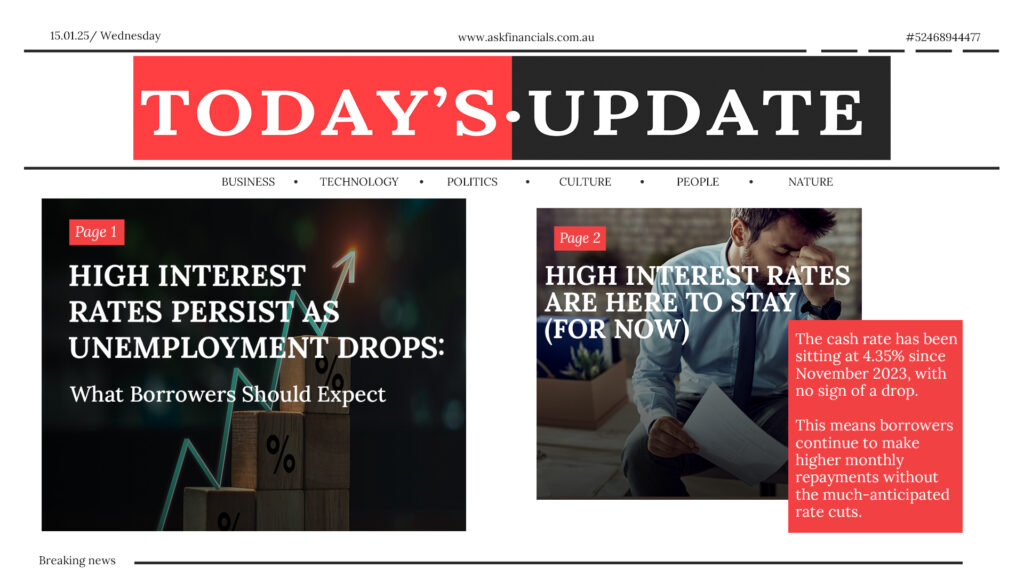

The extended period of high interest rates may persist for an additional period, as it has been in effect since November 2023, when the interest rate reached 4.35%.

Mortgage proprietors are currently required to make additional repayments.

This article explores the borrower’s experience with low unemployment in Australia and the potential long-term consequences of delayed cutbacks.

Has anything changed for borrowing?

For mortgage borrowers, the announcement might cause problems as more increasing payment quarters result from the lack of interest rate drops. While many borrowers have adjusted to the higher cash rate, refinancing prospects have not been present. As things stand, both lenders and borrowers should be careful, as any further delays would make it impossible to get a good deal on a new loan.

“In repaying debts, households continue to perform due to savings attained from the pandemic alongside cushioning the impact of high living expenses,” said ANZ economist Madeline Dunk. The low unemployment rate relieves some pressure on the RBA to adjust cash rates.

Managing the Debt during Prolonged Regime of High Rates

While it is difficult to estimate future rate cuts, household borrowers should take a proactive approach toward managing their finances. At this time, it may be prudent to evaluate the conditions of the existing loan and search for fixed rate options in order to ensure stability. And building a buffer

What does it matter that the RBA is being so careful?

RBA is equally careful with removals by cutting rates early enough as it strives to maintain inflation within acceptable boundaries while seeking growth in the economy. Given the strong employment and wage growth, the RBA Bank is therefore anticyclical to the economy overheating and thus unlikely to cut rates anytime soon.

What’s Next for the Housing Market?

With rates remaining the same for some time now, it appears that the housing market will be fairly dormant. Property prices are expected to not fluctuate significantly, which allows for first-time buyers to enter the market, however, high mortgage rates are likely to suppress demand. For the older homeowners, it is advisable to fix terms now, making it easier for them to cope with possible long periods of change later on.

In the case of current homeowners, the main objective should be to settle for a better deal and brace themselves for long-term rate changes. Even though there is a chance of rate cuts at some point eventually, no one really knows when that relief will come, and it’s extremely important to get ready for enduring financial chaos for however long that takes.

Australia’s paramount employment market has compounded the difficulty of rate cuts in the medium term. Borrowers have to deal with the high-interest period for longer. Careful financial management, wise refinancing, and anticipating financial rate changes will be essential to reduce the cost of waiting.

At ASK Financials, we consistently strive to provide borrowers with the most current information, defying common misconceptions.We give sound advice on the complexity of the modern world and solve all your financial matters.Contact us today for your financial security.