On Tuesday morning, NAB took up to 65 basis points off the stated fixed rates for its range of premium packaged mortgages.

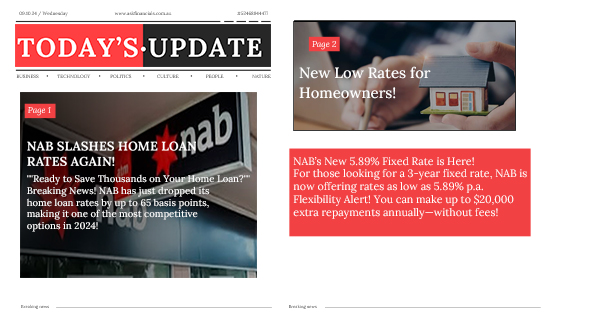

It now has rates as low as 5.89% p.a. for homeowners who pay back both the capital and the interest.

For those who agree to a three-year fixed rate, that is the lowest interest rate the bank will give on a home loan package designed just for them.

People who borrow money at a fixed rate Individuals with a tailored home loan can make up to $20,000 in extra payments each year without being charged extra fees. They can also choose to split their mortgage interest rate.

The rate cut by NAB comes just a few days after the bank changed its prediction for the first RBA cash rate cut from May 2025 to February 2025.

For those keeping an eye on the market, the big four bank is now the first of its peers to lower the rates on second homes in 2024. This comes after lowering rates on many of the same products in July.

How do NAB’s new lower home loan rates stack up against the best rates on the market?

Its new top rate is now the same as Westpac’s lowest rate, but it’s not as good as many of the rates listed by smaller Australian lenders.

The best interest rate on a mortgage right now seems to be 4.99% p.a. (6.15% p.a. comparison rate*), which is what tiny mutual SWSBank’s “special” 3 year fixed rate loan for people borrowing between $800,000 and $2.5 million promises.

The next best rate is from Macquarie, a financial bank, and it is 5.39% p.a. for three, four, and five years. This is lower than the comparison rate of 4.95% p.a.

The best variable rate deal right now is at Arab Bank, where you can get a Basics Home Loan with an interest rate of 5.75% p.a. (5.88% p.a. comparison rate*) if you borrow with a loan-to-value ratio (LVR) of 60% or less.

Homeowners can now get better rates on NAB home loans.

If you’re looking for a house or want to refinance your owner-occupier mortgage, NAB has some great new rates for you these days:

| Fixed Term | Old Rate | New Rate | Change% points |

| 1-years | 6.69% | 6.29% | -0.40 |

| 2-years | 6.59% | 6.04% | -0.55 |

| 3-years | 5.99% | 5.89% | -0.10 |

| 4-years | 6.74% | 6.24% | -0.50 |

| 5-years | 6.79% | 6.29% | -0.50 |

With this change, NAB’s rate is now the same as those from Commonwealth Bank (CBA) and Westpac. ANZ is now the only big lender with a three-year fixed rate that is still above 6%.

Big four banks: lowest advertised rates

| Loan Type | CBA | Westpac | NAB | ANZ |

| 1-year | 6.39% | 6.09% | 6.29% | 6.69% |

| 2-years | 6.29% | 5.89% | 6.04% | 6.54% |

| 3-year | 5.89% | 5.89% | 5.89% | 6.59% |

| 4-year | 6.29% | 5.89% | 6.24% | 6.74% |

| 5-year | 6.69% | 5.89% | 6.29% | 6.84% |

| Variable | 6.15% | 6.44%

2yrs+ then 0.4% pts |

6.79% | 6.14%* |

Competitive prices based on market trends.

NAB’s three-year fixed rate drop follows Macquarie Bank’s recent rate fall to 5.39%. Despite the recent cut, NAB still trails below the market’s lowest rate, which is 4.99% given by SWS Bank.

This move brings NAB’s lowest three-year fixed rates in line with its major bank competitors, CBA and Westpac’s lowest three-year rates.

Unwilling to lock in rates, borrowers

Borrowers are still not very interested in fixed rates, even though NAB’s fixed rate is now more competitive.

According to ABS data, only 2% of new and refinanced loans chose a fixed rate in August. Many borrowers would rather stick with variable rates in anticipation of possible RBA cash rate reductions later this year.

Pros and Cons of Long-Term Solutions

Fixing a home loan may provide some measure of tranquillity; however, it is not always the optimal option.

Frequently, fixed rates are associated with reduced flexibility, such as restricted avenues for additional repayments and the absence of an offset account.

The current rate reduction should serve as a “wake-up call” for householders to determine whether their current rates are higher than those offered to new debtors and to contact their lender to enquire about the possibility of a rate match.

A split loan strategy could be attractive to certain individuals.

For clients hesitant to lock into a fixed rate, a split loan could offer a sensible alternative. This strategy allows a segment of the loan to be fixed, ensuring stability, while the other segment remains variable, giving borrowers the opportunity to benefit from potential future rate reductions.

As fixed rates continue to decline across the industry, this presents a perfect opportunity for brokers to help clients reevaluate their mortgage choices. A minor decrease in interest rates can result in significant savings throughout the duration of the loan, potentially saving clients hundreds or even thousands of dollars.

Secure your lowest home loan rates with ASK Financials

Now is the ideal moment to act, as NAB and other lenders have reduced their rates. ASK Financial is available to assist you in securing the most favourable terms, whether you are purchasing your first property, refinancing, or simply investigating alternative options. Our experts will provide you with guidance throughout the procedure, ensuring that you maximise your savings.

Prepared to save? Reach out to ASK Financial today!